原文链接:http://tecdat.cn/?p=12111

在本文中,我将向您展示如何模拟股票价格的Heston随机波动率模型。

Heston模型是针对具有随机波动性的期权,并于1993年申请了债券的货币期权。对于固定的无风险利率![]() ,其描述为:

,其描述为:

![]()

通过使用这种模型,可以得出欧洲看涨期权的价格 。

这是函数的描述。

callHestoncf(S, X, tau, r, v0, vT, rho, k, sigma){

# S = Spot, X = Strike, tau = time to maturity

# r = risk-free rate, q = dividend yield

# v0 = initial variance, vT = long run variance (theta)

# rho = correlation, k = speed of mean reversion (kappa)

# sigma = volatility of volatility

}现在,进行蒙特卡洛定价。我们将为3个欧洲看涨期权定价![]() ,具有3种不同的执行价格。我们在15年中使用100000个模拟,每个月进行一次。以下是对仿真有用的参数:

,具有3种不同的执行价格。我们在15年中使用100000个模拟,每个月进行一次。以下是对仿真有用的参数:

#Initial stock price

S0 <- 100

# Number of simulations (feel free to reduce this)

n <- 100000

# Sampling frequency

freq <- "monthly"

# volatility mean-reversion speed

kappa <- 0.003

# volatility of volatility

volvol <- 0.009

# Correlation between stoch. vol and spot prices

rho <- -0.5

# Initial variance

V0 <- 0.04

# long-term variance

theta <- 0.04

#Initial short rate

r0 <- 0.015

# Options maturities

horizon <- 15

# Options' exercise prices

strikes <- c(140, 100, 60)为了使用模拟Heston模型,我们首先需要定义如何进行模拟。

此函数提供一个包含2个成分的列表,每个成分包含模拟的随机高斯增量。

# Stochastic volatility simulation

sim.vol <- simdiff(n = n, horizon = horizon,

frequency = freq, model = "CIR", x0 = V0,

theta1 = kappa*theta, theta2 = kappa,

theta3 = volvol, eps = shocks[[1]])

# Stock prices simulation

sim.price <- simdiff(n = n, horizon = horizon,

frequency = freq, model = "GBM", x0 = S0,

theta1 = r0, theta2 = sqrt(sim.vol),

eps = shocks[[2]])现在,我们可以使用3种不同的

计算期权价格。

# Stock price at maturity (15 years)

print(results)

strikes mcprices lower95 upper95 pricesAnalytic

1 140 25.59181 25.18569 25.99793 25.96174

2 100 37.78455 37.32418 38.24493 38.17851

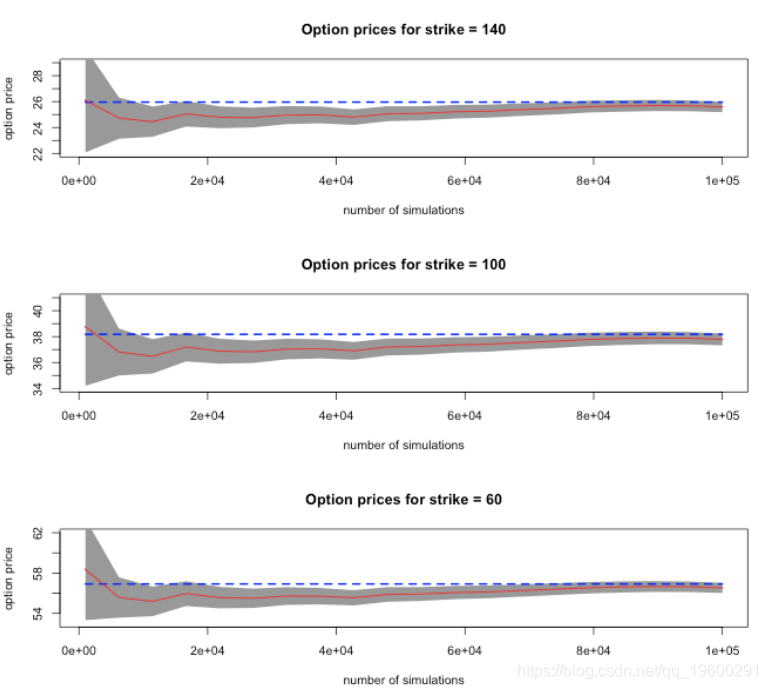

3 60 56.53187 56.02380 57.03995 56.91809从这些结果中,我们看到这三个选项的蒙特卡洛价格与使用函数(直接使用公式来计算价格)计算出的价格相当接近。95%的置信区间包含理论价格。

下面是期权价格,作为模拟次数的函数。计算出的理论价格用蓝色绘制,蒙特卡洛平均价格用红色绘制,阴影区域表示均值(蒙特卡洛价格)周围的95%置信区间。

![]()